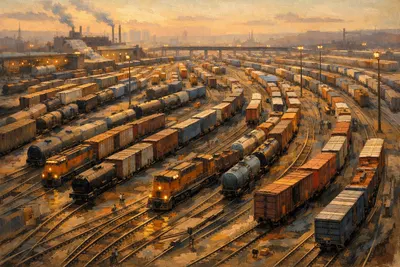

Union Pacific owns thirty thousand miles of track that nobody else can build

The largest railroad in the western United States earns .8 billion a year hauling freight on infrastructure that would cost over billion to replicate. At 22 times earnings, the price is fair for a business this durable.

Thirty thousand miles of track that nobody else can build

If you wanted to compete with Union Pacific, you would need to lay 32,000 miles of railroad track across the western two-thirds of the United States. You would need rights of way through cities, across rivers, over mountains, and through deserts. You would need decades of regulatory approval. And you would need to spend something in the range of $100 billion to $200 billion, conservatively, just to recreate the physical infrastructure.

Nobody is going to do this. That is the moat.

The business in plain terms

Union Pacific hauls things. Coal, grain, chemicals, automobiles, intermodal containers, lumber, and industrial products ride on its trains from the ports of Los Angeles and Long Beach to Chicago and everywhere in between. In 2025, the company generated $24.5 billion in revenue and about $6.8 billion in net income, which works out to roughly $11.29 per share after the 8% growth in EPS over the prior year.

Revenue carloads grew 7% in Q1 2025. Freight car velocity hit 225 daily miles per car, a record. The operating ratio, which is the railroad industry's preferred measure of efficiency (lower is better), came in at 60.7%. That means for every dollar of revenue, Union Pacific spent about 61 cents running the operation and kept the rest. A decade ago, that ratio was closer to 65%. The improvement is real and reflects years of investment in precision-scheduled railroading.

Free cash flow for 2025 was $5.5 billion. For a capital-intensive business, that is a strong number. Railroads require constant reinvestment in track, locomotives, and rolling stock, but the return on that investment has been excellent. Union Pacific has spent heavily and still generated more cash than it needs.

Why railroads are good businesses

A train can move one ton of freight about 500 miles on a single gallon of fuel. A truck cannot come close. This fuel efficiency gives railroads a structural cost advantage on long-haul, heavy freight. It also gives them a natural environmental advantage, which matters more each year as shippers face pressure to reduce carbon emissions.

The economics favor consolidation. The United States has only four major freight railroads (two in the West, two in the East), and the regulatory environment makes new entry essentially impossible. Union Pacific and BNSF (owned by Berkshire Hathaway) dominate the western half of the continent. They compete with each other on some routes and hold effective monopolies on others.

This duopoly structure means pricing power. When a chemical manufacturer in Houston needs to ship product to a customer in Oregon, there may be only one railroad that serves both endpoints. The shipper can truck the load instead, but for bulk commodities over long distances, the math almost always favors rail.

Capital allocation

Management authorized a new $4.5 billion share buyback program in early 2025, on top of the ongoing repurchase activity. The share count has been declining steadily, dropping from roughly 680 million diluted shares in 2015 to about 600 million today. That 12% reduction in shares outstanding, combined with modest revenue growth and margin improvement, has compounded per-share earnings nicely over the past decade.

The dividend yields around 2.2% and has grown every year. Together, buybacks and dividends return the majority of free cash flow to shareholders. Capital expenditures run about $3.5 billion to $4 billion annually, which is the cost of maintaining and gradually improving 32,000 miles of track, bridges, tunnels, and signal systems.

One thing worth noting: railroads carry substantial debt. Union Pacific has about $33 billion in long-term debt, which sounds alarming until you consider that the debt is well-termed, the interest coverage is comfortable, and the business generates highly predictable cash flows. Railroads have been among the most reliable debt issuers in American corporate history for good reason. The assets are real, the cash flows are steady, and the competitive position is nearly permanent.

What could go wrong

Economic downturns reduce freight volumes. Railroads are cyclical businesses, and their revenue tracks industrial production, consumer spending, and trade flows. In a recession, carloads drop and pricing power weakens temporarily. Union Pacific's volume declined in 2020 and again during the 2023 freight recession before recovering.

Regulation is a perennial concern. The Surface Transportation Board oversees railroad rates, and there are periodic political calls for stricter oversight, particularly after service disruptions or safety incidents. The 2023 East Palestine derailment (at Norfolk Southern, not Union Pacific) reminded the industry and the public that railroads operate under a microscope.

Labor relations require constant attention. Railroads operate with unionized workforces, and contract negotiations can be contentious. A national rail strike was narrowly averted in 2022 through federal intervention. Labor costs are a major expense, and any disruption to service can damage customer relationships for years.

Coal volumes continue their long decline as utilities shift to natural gas and renewables. Coal once represented a quarter of Union Pacific's revenue; today it is closer to 10%. The loss has been gradual and partly offset by growth in intermodal and industrial segments, but it is a headwind that has not finished blowing.

Valuation and the owner's return

At a stock price near $252 and roughly 600 million diluted shares, the market cap is approximately $151 billion. On trailing earnings of about $6.8 billion, that is roughly 22 times earnings. For a business with this kind of durability, limited competition, and consistent cash generation, 22 times is a reasonable price. It is not a bargain, but it is not demanding perfection either.

The combination of low-single-digit revenue growth, ongoing margin improvement, and steady share count reduction could deliver earnings growth of 7% to 9% per year. Add the 2.2% dividend yield, and total shareholder returns in the range of 9% to 11% are plausible if the current multiple holds. That is a fair deal for a business that will almost certainly be operating a century from now.

Railroads are not exciting. They do not disrupt anything. They move heavy things from one place to another, slowly and reliably, and they have done so for 150 years. Sometimes the best investments are the ones that bore everyone else.

Warren Bigfoot is a classic value investor who focuses on businesses with durable competitive advantages, strong balance sheets, and rational capital allocation. He ignores macroeconomic noise and market volatility, choosing instead to view market drops as opportunities to acquire wonderful companies at fair prices. His holding period is typically measured in years, if not decades.

View all articles →