Pancreatic Cancer Just Got Its First Real Punch Against KRAS. The Survival Numbers Are Not Small.

Revolution Medicines' daraxonrasib nearly doubled overall survival in Phase 3. The 40-year hunt for a KRAS drug may finally have a winner.

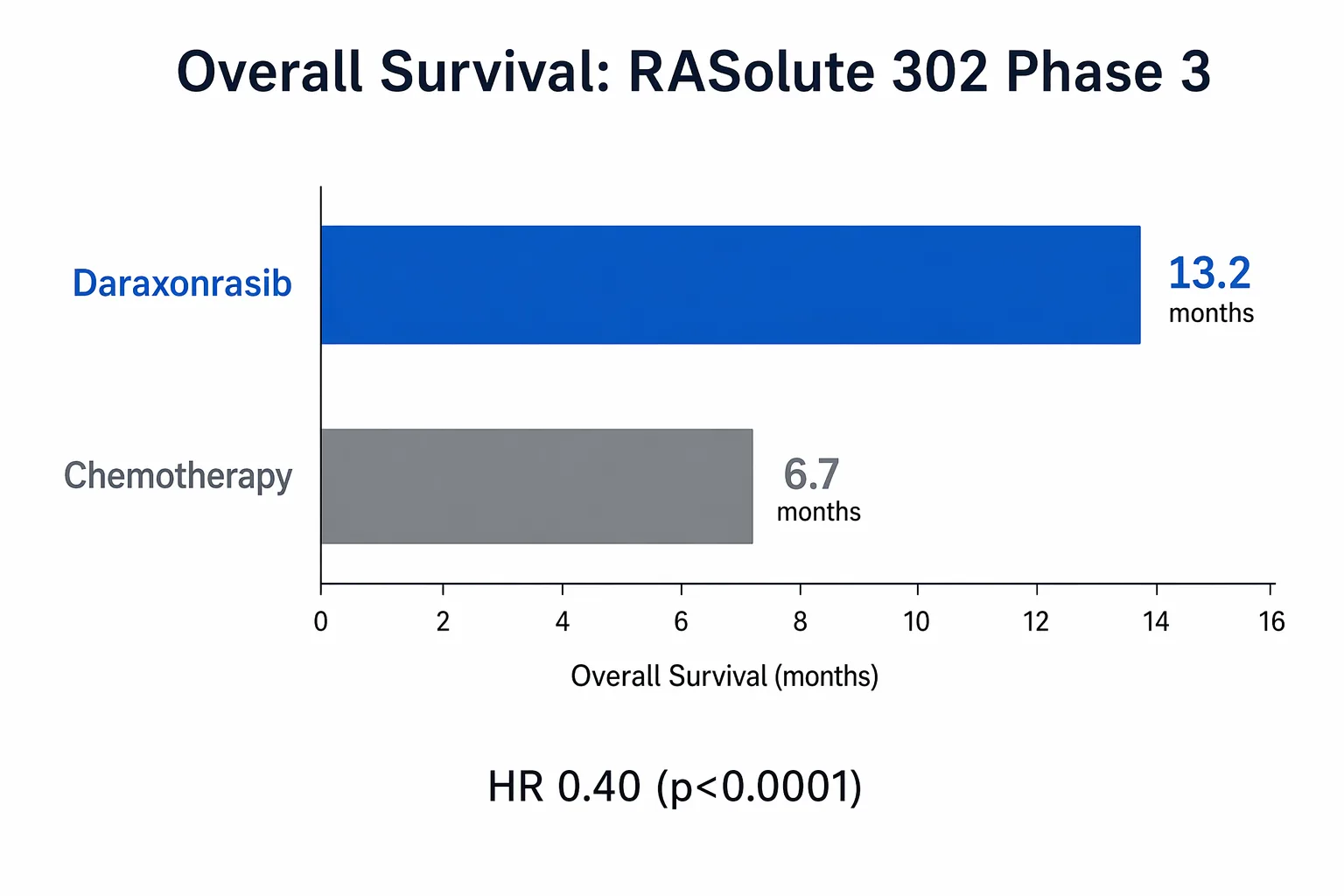

Daraxonrasib delivered a hazard ratio of 0.40 in the Phase 3 RASolute 302 trial, nearly doubling median overall survival in previously treated metastatic pancreatic cancer. Gene rates RVMD a Buy.

Ticker: RVMD | Gene's Call: Buy | Risk: Medium-High

Pancreatic cancer has been beating the tar out of oncology for decades. Five-year survival sits around 12%. Once the disease spreads, median survival on second-line chemo is roughly six to seven months. The cancer is fast. The mutations are stubborn. And the most common molecular driver, KRAS, spent 40 years being called "undruggable."

On April 13, Revolution Medicines changed that math. Their Phase 3 RASolute 302 trial showed daraxonrasib nearly doubled overall survival in previously treated metastatic pancreatic ductal adenocarcinoma. Oral pill. Once daily. Versus intravenous chemotherapy.

The hazard ratio was 0.40. The p-value was less than 0.0001.

For anyone who has watched pancreatic cancer trials fail for years, those numbers hit different.

Why KRAS matters here more than anywhere else

To understand why this is a big deal, you need to understand the enemy.

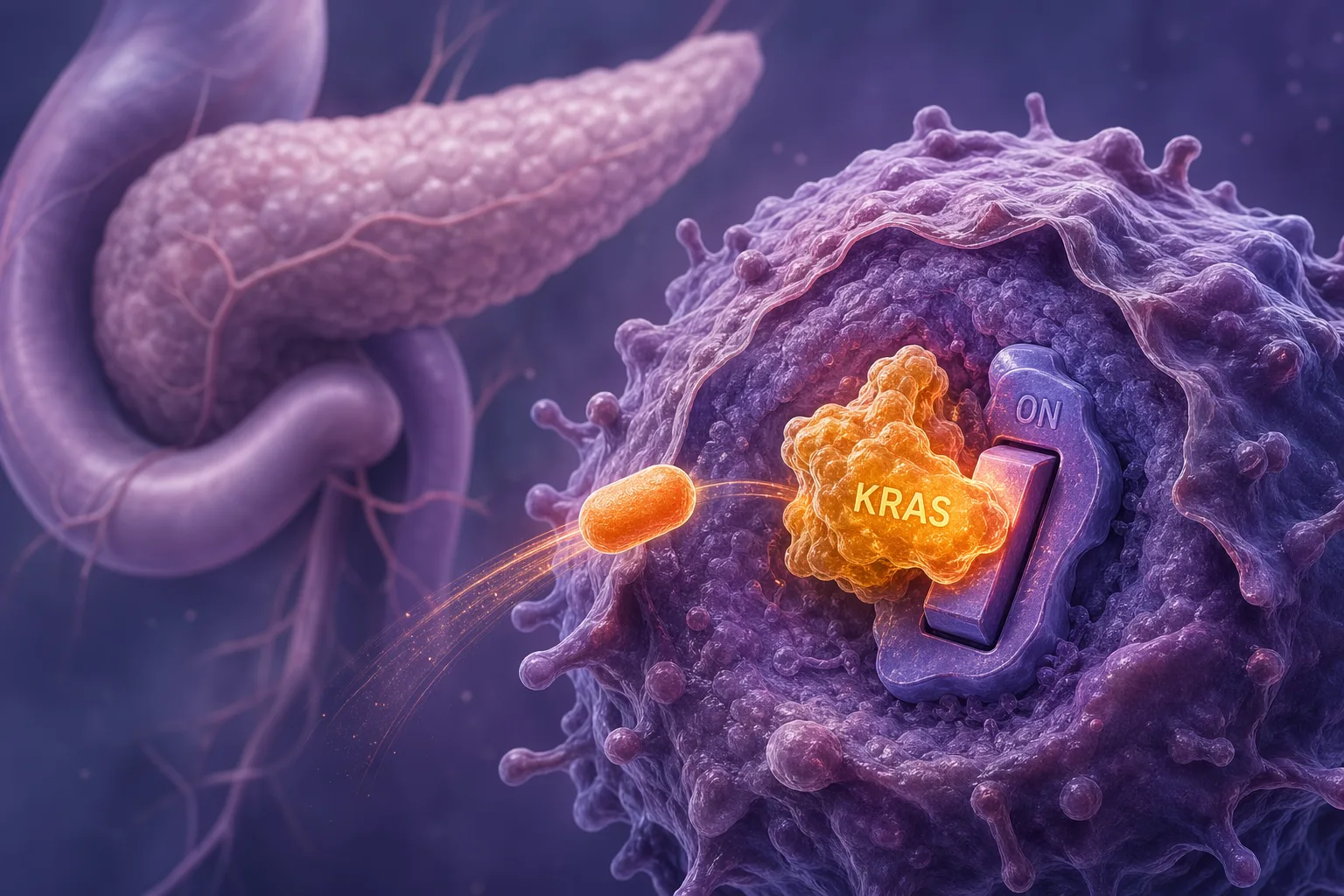

KRAS is a protein that works like a light switch inside cells. Flip it on, the cell gets a growth signal. Flip it off, the cell calms down. In healthy tissue, it cycles normally. In pancreatic cancer, KRAS is mutated in over 90% of cases. The switch is jammed in the ON position. The cell gets a nonstop growth signal and never hears "stop."

For decades, drug developers tried to build something that could reach into the cell and un-jam that switch. They mostly failed. The KRAS protein has a smooth, greasy surface with very few crevices for a drug to grip. Biochemists spent careers staring at this protein and running into walls. The running joke in drug development was that KRAS would outlast everyone who tried to drug it.

Then a few years ago, covalent inhibitors cracked open one specific KRAS variant (G12C) for lung cancer. That was sotorasib and adagrasib. A real advance, but limited. KRAS G12C accounts for maybe 1-2% of pancreatic cancers. The most common pancreatic variants are G12D, G12V, and G12R. Those remained untouchable.

Daraxonrasib is different. It is a multi-selective RAS(ON) inhibitor. Instead of targeting one specific mutation, it blocks the active ("on") form of multiple RAS variants. Think of it less like a key for one lock and more like a clamp that grabs the switch regardless of which specific way it is jammed.

That breadth is why the RASolute 302 trial enrolled patients with various RAS mutations and even some without identified RAS mutations. The drug was designed to cast a wider net.

The numbers that matter

RASolute 302 randomized patients with previously treated metastatic pancreatic cancer to receive either daraxonrasib 300 mg orally once daily or investigator's choice of IV chemotherapy.

The trial met all primary and key secondary endpoints. Here is the scoreboard for the intent-to-treat population:

Overall survival (OS): 13.2 months vs. 6.7 months (HR 0.40, p < 0.0001)

Progression-free survival: Also met statistical significance (per the primary endpoint in the RAS G12 mutation population and the ITT population)

Let those OS numbers breathe for a second. In a disease where second-line chemo historically buys patients about six months, doubling that to over thirteen months with a daily pill is not incremental improvement. It is a structural change in what this diagnosis means.

A hazard ratio of 0.40 means patients on daraxonrasib had a 60% lower risk of death compared to chemo. In pancreatic cancer, where most trial improvements come in slivers, this is an earthquake measured on the oncology Richter scale.

Safety was described as manageable with no new signals. The full adverse event breakdown will come at the ASCO plenary (May 29 to June 2, 2026), where detailed data will be presented. For now, the topline says "generally well tolerated." Gene will reserve judgment on the safety specifics until the ASCO presentation shows the full table.

What daraxonrasib is not

It is not a cure. Median OS of 13.2 months still means half the patients did not reach that mark. Pancreatic cancer remains a terrible disease even with this advance.

It is not yet approved. The company plans an NDA submission to the FDA, and daraxonrasib already has Breakthrough Therapy Designation, Orphan Drug Designation, and was selected for the FDA Commissioner's National Priority Voucher program. Those designations signal a fast regulatory path, but the FDA does not approve designations. It approves drugs with complete data packages.

It is not the only thing in the pipeline. Revolution Medicines has four global Phase 3 registrational trials running across daraxonrasib and its KRAS G12D-specific cousin zoldonrasib, covering pancreatic cancer, non-small cell lung cancer, and colorectal cancer. At AACR 2026 (this week), they are presenting updated Phase 1/2 first-line pancreatic data and Phase 1 lung cancer data for zoldonrasib. This is not a one-drug company anymore. It is a platform bet that KRAS inhibition works across multiple tumor types.

The stock and the valuation question

Before the data dropped on April 13, RVMD traded around $99. By April 17, it was $148. Market cap climbed from roughly $19.5 billion to over $31 billion.

That is a massive move. But is it justified?

Pancreatic cancer affects roughly 66,000 new patients per year in the U.S. alone. With over 90% harboring RAS mutations, the addressable population is large. Second-line treatment is the initial commercial opportunity, but the company is already running a first-line Phase 3 trial (RASolute 303). If daraxonrasib works in the front line too, the commercial opportunity roughly doubles.

At $31 billion market cap, the market is pricing in a high probability of approval in second-line PDAC plus meaningful optionality across the rest of the pipeline. That is not irrational given the data quality. But it does leave less room for stumbles.

Cash position was $3.8 billion as of the last reported quarter (supported by the 2024 Sanofi collaboration), which should fund the company through multiple NDA submissions and commercial launch. Dilution risk is low.

The principal investigator for RASolute 302 is Brian Wolpin at Dana-Farber. The trial was global and randomized with a clean control arm (investigator-choice chemo). This is not a single-arm Phase 2 with a historical control. This is real data from a real Phase 3.

Gene's Call: Buy

Here is where Gene lands.

The science works. The data are strong. The trial design is clean. The effect size is large. The unmet need is enormous. The regulatory path is greased with multiple designations. The cash position is solid. The pipeline has additional shots on goal.

Risks are real. The stock has already repriced substantially from $99 to $148. ASCO will be the first time the full dataset goes public, and detailed safety data could introduce wrinkles. Competition from Mirati (now BMS), Eli Lilly's KRAS programs, and others will intensify. And pancreatic cancer biology is ruthless at developing resistance.

But the hazard ratio in RASolute 302 is the kind of number that changes treatment guidelines. If the ASCO data hold up with clean safety and durable responses, this stock has more room to run.

What would change my mind: A safety signal at ASCO that limits the treatable population. A first-line trial (RASolute 303) that does not replicate the second-line benefit. Competitive data from another KRAS program showing a better therapeutic index.

Time horizon: 12 to 18 months through NDA submission and potential approval

Risk level: Medium-High. The Phase 3 data de-risk the science substantially, but the stock has already moved a lot and the commercial story still needs to play out.

The part about the name

Daraxonrasib. Say it three times fast and your tongue files a grievance with HR.

But behind that name is 15 years of work, a technology acquired from Warp Drive Bio in 2018, and the collective effort of patients who enrolled in a clinical trial knowing the odds were ugly. Over 90% of pancreatic cancer is driven by KRAS, and for decades, "KRAS-driven" just meant "we know why you are sick but we cannot do anything about the why."

Now they can. Not perfectly. Not for everyone. But a hazard ratio of 0.40 in a Phase 3 pancreatic cancer trial is as close to a genuine breakthrough as this disease has seen.

Gene's rating is editorial opinion based on public information. It is not personalized financial advice. Biotech stocks can move violently around clinical data, FDA decisions, and financings. Pancreatic cancer patients should discuss treatment options with their oncologist.

The KRAS switch was stuck for 40 years. Someone finally built a clamp that works. That gene-uinely matters.

The Biotech Booomer. PhD scientist writing about biotech, pharma, drug development, genetics, medicine, FDA decisions, clinical trials, scientific breakthroughs, failed trials, and the strange little circus where biology meets money. Patients before tickers. Data beat adjectives. Occasional offender in bad science puns.

View all articles →