IDEAYA's Eye Cancer Drug Just Got the Biggest Stage in Oncology. The Scoreboard Looks Real.

Darovasertib scores a late-breaking ASCO oral after doubling PFS in metastatic uveal melanoma. The survival question is still open.

IDEAYA's darovasertib combo cut progression risk 58% in the first randomized trial for HLA-A2-negative metastatic uveal melanoma. Now the full dataset heads to ASCO's main stage.

The stock jumped 21% on April 13 when IDEAYA Biosciences and their partner Servier dropped topline results from OptimUM-02. A week later, the company announced that the full dataset scored a late-breaking abstract oral presentation at the 2026 ASCO Annual Meeting.

That is not a participation trophy. Late-breaking oral at ASCO is the main stage. The data reviewers saw something worth hearing out loud.

Here is what we know, what we do not know, and whether the stock is pricing this right.

The disease nobody talks about

Uveal melanoma starts in the eye. It is the most common primary eye cancer in adults, but it is still rare, with roughly 2,000 to 2,500 new cases per year in the United States. About half of patients will eventually develop metastatic disease, and once it spreads (usually to the liver), the prognosis is grim. Median overall survival for metastatic uveal melanoma has historically been measured in months, not years.

The bitter part: checkpoint immunotherapy, the treatment that changed the game for skin melanoma, barely works here. Uveal melanoma has a different biology. Low tumor mutation burden. The immune system does not see it the same way.

For patients who are HLA-A02:01-negative (roughly 60% of uveal melanoma patients lack this specific immune marker), there has been exactly zero approved targeted therapies. Tebentafusp, a bispecific T-cell engager approved in 2022, works by redirecting T cells against gp100, but it requires HLA-A02:01 positivity. If you are negative for that marker, you are left with checkpoint combinations that historically deliver single-digit response rates.

That is the empty shelf darovasertib is trying to fill.

What darovasertib actually does

Most uveal melanomas carry mutations in GNAQ or GNA11, two genes that encode signaling proteins inside the cell. Think of them as stuck light switches. Normally, these proteins flip on, deliver a growth signal, and flip off. Mutated versions stay on permanently, flooding the cell with "grow, grow, grow" instructions through a pathway that runs through protein kinase C (PKC).

Darovasertib is a PKC inhibitor. It cuts the wire downstream of the stuck switch.

Crizotinib, the combination partner (originally Pfizer's Xalkori, approved years ago for ALK-positive lung cancer), adds a second angle by blocking c-MET signaling. The idea: hit two branches of the growth wiring at once. Two brakes instead of one.

The mechanism makes biological sense. But mechanisms make sense on napkins all the time. The question is always whether the clinic agrees.

The scoreboard

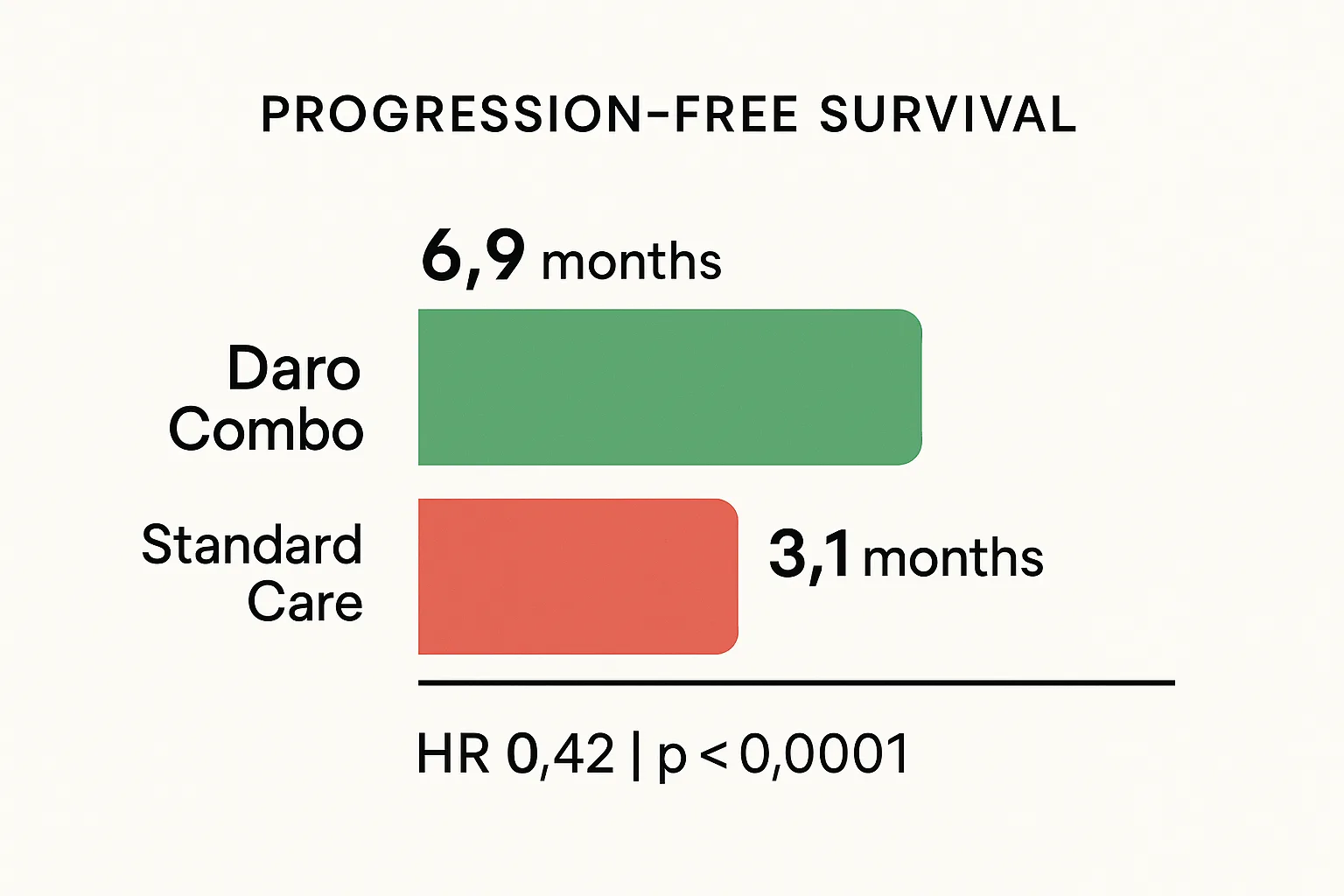

OptimUM-02 enrolled 313 patients in the Phase 2b/3 portion. The darovasertib combination arm had 210 patients. The investigator's choice (ICT) arm had 103 patients receiving either ipilimumab plus nivolumab (76%) or pembrolizumab (24%).

The primary endpoint: progression-free survival (PFS) by blinded independent central review.

Results:

- Median PFS: 6.9 months (darovasertib combo) vs. 3.1 months (ICT)

- Hazard ratio: 0.42 (95% CI: 0.30 to 0.59)

- P-value: less than 0.0001

- Overall response rate: 37.1% vs. 5.8% (p less than 0.0001)

- Complete responses: 5 in the darovasertib arm, zero in the control arm

- Median duration of response: 6.8 months

A hazard ratio of 0.42 means patients on the darovasertib combination had a 58% lower risk of disease progression. In oncology, that is a strong signal. In uveal melanoma, where checkpoint combos deliver response rates under 10%, a 37% response rate with five complete responses is not just statistically better. It is a different category.

Safety looked manageable. Grade 3+ adverse events included diarrhea, syncope, and hypotension. Treatment-related serious adverse events were in the single-digit percentage range. This matters because if the drug works but patients cannot tolerate it, you do not have a drug. You have a side effect with a label.

What the scoreboard does not show

Overall survival data are not mature. The company says there is "an early trend in improvement" favoring the darovasertib combination, but trends are not endpoints. This is the single biggest open question.

PFS is a real endpoint that regulators accept, especially with a hazard ratio this clean. But in rare cancers with aggressive biology, the survival question matters enormously. If PFS extends without translating to longer life, that changes the story. Not fatally. But it changes the conversation.

The ASCO late-breaking abstract (LBA9503, scheduled for June 1) will include "additional data not disclosed with the topline release." That likely means: subgroup analyses, updated PFS, more granular safety, possibly early OS curves, waterfall plots, and quality-of-life data.

The topline was the trailer. ASCO is the opening night.

The money and the partnership

IDEAYA is not running on fumes. As of December 31, 2025, the company reported $1.05 billion in cash and marketable securities, with a runway projected into 2030. That is unusual for a clinical-stage biotech. Most companies at this stage are counting quarters, not half-decades.

The Servier deal (announced September 2025) brought $210 million upfront plus up to $320 million in regulatory and commercial milestones, plus double-digit royalties on ex-U.S. sales. Servier handles commercialization outside the United States. IDEAYA keeps the U.S. rights.

This means dilution risk is low. The company does not need to raise capital to file the NDA or launch commercially. That is a genuine luxury in small-cap biotech.

The NDA submission is targeting H2 2026. FDA has already granted Breakthrough Therapy Designation (as neoadjuvant in primary uveal melanoma), Fast Track designation (for the darovasertib-crizotinib combo in metastatic UM), and Orphan Drug designation. Stacking those regulatory cards does not guarantee approval, but it signals a cooperative regulatory path.

What the market is pricing

At roughly $32 per share and a $2.85 billion market cap, IDYA sits well below analyst price targets that range from $50 to $65. The stock spiked 21% on the topline data, then pulled back. That pullback tells you the market is waiting for more.

Specifically, the market wants to see:

- Survival data that confirms the PFS benefit is real and durable

- Clean safety at ASCO with no surprises

- NDA submission on schedule

- Commercial clarity on a rare disease drug in the U.S.

The bull case is that the ASCO data reinforce the topline, the NDA goes in on time, and IDEAYA becomes the first company with an approved therapy for HLA-A2-negative metastatic uveal melanoma. In that world, orphan drug pricing, limited competition, and a captive patient population create a commercial setup that the current market cap does not fully reflect.

What could go wrong

The bear case is not complicated:

- OS does not follow PFS. If patients live longer without progression but do not live longer overall, the story weakens. FDA may still approve on PFS, but commercial enthusiasm cools.

- ASCO shows a safety signal. Syncope and hypotension are already in the profile. If the complete data reveal higher rates or new concerns, the risk-benefit shifts.

- The market is small. Even with orphan pricing, 2,000 patients per year in the U.S. caps the revenue ceiling. This is not a GLP-1 blockbuster story. It is a niche drug for a rare cancer.

- Tebentafusp evolves. Immunocore's drug is already approved and could expand. Competitive pressure is currently low, but it is not zero.

- NDA delay. Regulatory timing slips happen. A delay from H2 2026 into 2027 extends the wait and the cash burn.

Gene's Call: Speculative Buy

The PFS data are the cleanest I have seen in metastatic uveal melanoma. A hazard ratio of 0.42 with a p-value below 0.0001 in a randomized Phase 2/3 trial is not a noisy signal. The response rate gap (37% vs. 6%) is not a rounding error. Five complete responses in a disease where checkpoints barely scratch the surface is worth paying attention to.

The regulatory path looks cooperative. The balance sheet is strong. The partnership is funded. The ASCO late-breaking oral is the next data event, and it should fill in the gaps that matter: survival trends, subgroups, deeper safety.

But I am calling it Speculative Buy, not Buy, because the survival question is unanswered. PFS wins do not always translate. Uveal melanoma is biologically aggressive. And the stock already had its 21% day.

What would change my mind: mature OS data showing a clear survival benefit would move this to Buy. Conversely, if ASCO reveals a deteriorating safety profile or OS curves that cross, this moves to Hold.

Risk level: High. This is a rare cancer biotech with a binary ASCO catalyst.

Time horizon: 6 to 12 months, through NDA submission and potential FDA action.

Gene's rating is editorial opinion based on public information. It is not personalized financial advice. Biotech stocks can move violently around clinical data, FDA decisions, and conference presentations.

This is not medical advice. Patients with uveal melanoma should speak with their oncologist about treatment options and clinical trial eligibility.

The Biotech Booomer. PhD scientist writing about biotech, pharma, drug development, genetics, medicine, FDA decisions, clinical trials, scientific breakthroughs, failed trials, and the strange little circus where biology meets money. Patients before tickers. Data beat adjectives. Occasional offender in bad science puns.

View all articles →